6 things South Florida rental owners get wrong — and the truth from nearly 30 years managing 750+ units.

Own a rental in Broward, Palm Beach, or Miami-Dade? Let’s separate fact from fiction.

Owning a rental property in South Florida can be one of the smartest investments you’ll ever make — or one of the most stressful. The difference usually comes down to how it’s managed. Yet a lot of owners hesitate to bring in a professional property manager because of things they’ve heard rather than things that are true.

At Home Solutions Property Management, we’ve spent nearly three decades managing more than 750 rental units across Broward, Palm Beach, and Miami-Dade. We’ve heard every myth in the book. Let’s clear up the six biggest ones.

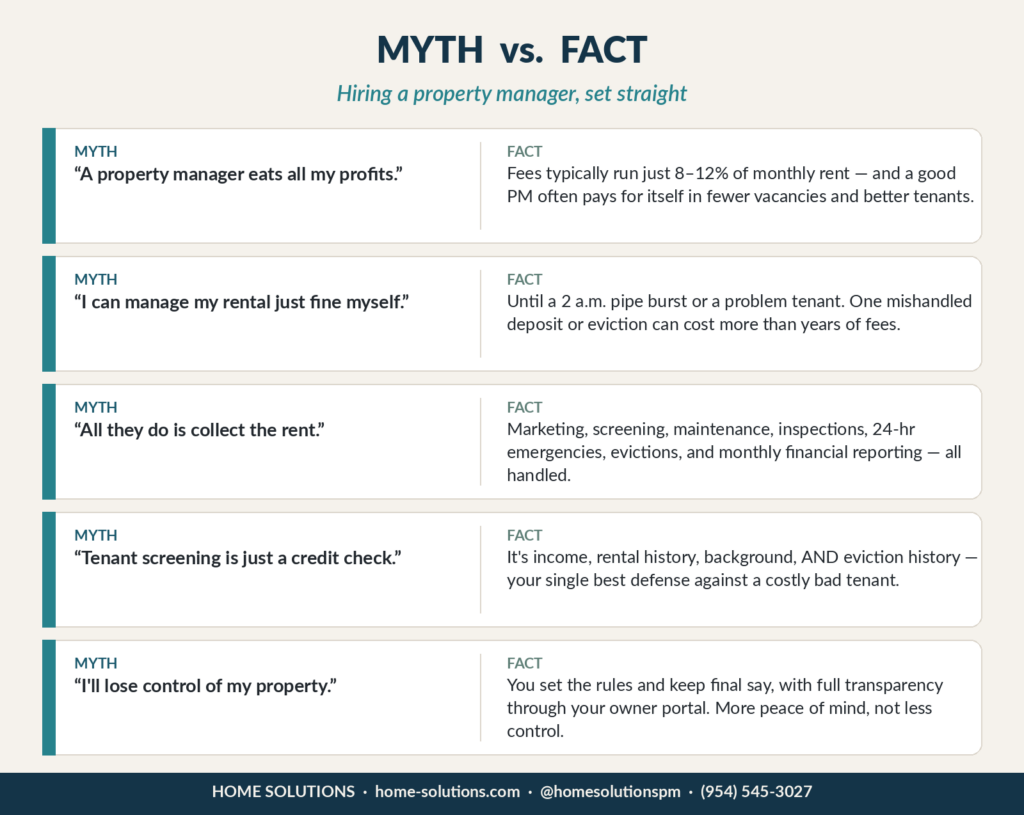

Myth #1: “A property manager will eat all my profits.”

This is the big one — and it’s backwards. In Florida, professional management typically runs 8–12% of the monthly rent. For that, a good manager often pays for itself: shorter vacancies, better-qualified tenants, on-time rent, and far fewer of the expensive mistakes that quietly drain a DIY landlord’s returns.

The real question isn’t “What does management cost?” — it’s “What is not having it costing me?”

Myth #2: “I can manage my own rental just fine.”

Plenty of owners do — right up until the 2 a.m. pipe burst, the tenant who stops paying, or the security-deposit dispute that lands in court. Florida’s landlord-tenant law (Chapter 83) is strict and specific, and a single mishandled notice, deposit return, or eviction can cost you more than years of management fees.

Professional management means those situations are handled the first time correctly — by people who do this every single day.

Myth #3: “All a property manager really does is collect the rent.”

Rent collection is the easy part. Behind the scenes, full-service management means marketing your property, screening applicants, coordinating maintenance, conducting inspections, handling 24-hour emergencies, managing evictions, and delivering clear monthly financial reporting — all through owner and tenant portals so nothing falls through the cracks.

Myth #4: “No one will care about my property the way I do.”

A good manager’s entire reputation — and income — depends on protecting your asset. That means vetted vendors, routine inspections, and documentation that catch small problems before they become five-figure repairs. You get a partner whose success is tied directly to the long-term health of your property.

Myth #5: “Tenant screening is just a quick credit check.”

Not even close. Proper screening layers income verification, rental history, background checks, and prior eviction history — and it’s your single best defense against a costly bad tenant. One bad placement can erase a year of rent in damage, lost time, and legal fees. This is where experience earns its keep.

Myth #6: “Hiring a property manager means I lose control.”

You actually gain clarity. You set the parameters — rent targets, approval thresholds, how you want issues handled — and you keep final say on the big decisions. With transparent monthly reporting and an owner portal, you’ll often know more about your property than you did managing it yourself. That’s more peace of mind, not less control.

Quick Answers: Owner FAQs

Q: How much does property management cost?

A: Most Florida management fees run 8–12% of monthly rent, often with a tenant-placement fee. We keep our pricing transparent and walk you through exactly what’s included — no surprise line items.

Q: What areas do you serve?

A: We manage single-family homes, condos, multi-unit dwellings, and small apartment buildings across Broward, Palm Beach, and Miami-Dade counties, from our home base in Wilton Manors.

Q: What happens if my tenant stops paying?

A: We handle it by the book. Florida has a defined legal process for non-payment, and we manage the notices and eviction steps correctly and promptly — protecting your property and your rights.

Q: How quickly can you rent my property?

A: It depends on the market and the unit, but professional marketing, fast showings, and thorough screening are how we minimize vacancy while still placing the right tenant. Ask us for a free rental analysis to see what your property should command.

“Owning a rental shouldn’t feel like a second job. Our whole approach is simple — protect the property, take care of the tenants, and give owners back their time and peace of mind.”

— Jodi Turbyfill, Owners, Home Solutions Property Management

Thinking About Hiring a Property Manager?

Start with a free, no-obligation rental analysis. We’ll tell you what your property should rent for in today’s South Florida market and exactly how we’d manage it — so you can make the call with real numbers in hand.

Let’s make your rental work for you — not the other way around.

👉 Get started with Home Solutions

Learn about our full-service property management.

Call us: (954) 545-3027

Follow us on Instagram: @homesolutionspm.

📍 Serving Broward, Palm Beach & Miami-Dade counties | Wilton Manors, FL

2. Grade and Foundation Cracks

2. Grade and Foundation Cracks